Stress Testing Loan and Deposit Prepayments

Recently, we discussed the growing importance of not only developing institutionally relevant assumptions derived from your bank’s own historical data, but also the importance of stress testing these assumptions to isolate the impact a movement in a single assumption can have on a bank’s interest rate risk.

In light of increased examiner scrutiny on bank assumptions, and subsequently stressing those assumptions, we here at AMG have added 2 new stress tests. These 2 new tests will focus on loan and deposit prepayment factors in order to give the BancPath user a clear understanding of the affect these assumptions can have on the bank’s interest rate risk profile.

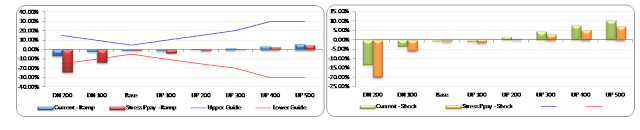

The first test we call the Prepayment Stress Factor. This test uses a Prepayment Stress Factor on loan prepayment speeds. This will generally have a NEGATIVE impact on the Interest Rate Risk Profile as rates decline (more dollars are repriced at lower rates) and as rates increase (fewer dollars are available to be repriced at higher rates). An example of this test is below where you can see the impact on Net Interest Income:

The second new stress test uses a Deposit Prepayment Stress Factor in conjunction with a Defined Prepayment Rate (either a default value or User Defined) to increase the expected forfeiture of Time Deposits in a rising rate environment. This will generally have a NEGATIVE impact on the Interest Rate Risk Profile as the probability for early withdrawals of time deposits increases. This is a simple test that applies an "across the board" prepayment rate. We would expect that actual prepayments would be much less severe as the likelihood of early withdrawals would ONLY occur on longer time deposits. See the effect on Net Interest Income below:

If you have any questions about this process, please don’t hesitate to contact us at Asset Management Group.