Does Cost of Funds Matter When Pricing Loans?

by AMG

Bankers live by the old 3-6-3 rule. Pay 3 on deposits, charge 6 on loans, and be on the golf course by 3 o'clock.

I have heard that tired old joke more times than I can count. I still chuckle at it, as I do all banker jokes (just don't make the "Banker's Hours" joke to my wife - she does not find it amusing). So while the days of getting in that much golf are long gone, does the basic pricing philosophy still have merit? Are we making this business way too complicated?

I get some version of this question on a regular basis. In fact, I would say that the majority of community banks still use dome form of what I call "cost plus" pricing. That is, to price a loan, you take your current cost of funds and add some spread to it based on the perceived risk level of the loan. If you get a request for a longer term fixed rate loan, then you find some way to match fund it and add your spread to that funding cost. In fact, this is exactly how I was taught to price loans earlier in my career. Our rule of thumb was to seek a spread of 4% - that was 3% to pay the bills, and that left us a roughly 1% profit (targeting a 1% R.O.A.).

There are several issues with this approach. I'll cover what I see as the 2 biggest problems.

1. Not all Margin is Created Equal

Focusing on a "cost plus" method to create margin leads us to take on more incremental risk. First, banks using this approach will invariably over-value loans and under-value their securities portfolio. Compared to their cost of funds, many banks barely make a profit. However, a 150 basis point spread over cost of funds on a short, highly liquid portfolio of agency bonds should not be compared directly to a 350 basis point spread over cost of funds on a commercial real estate loan portfolio. Which would you rather earn?

Second, and more problematic, is that this often leads to bank charging too much for short floating rate loans and too little for longer term fixed rate loans. Earlier this week I spoke with a bank that was pricing a large commercial real estate loan for a strong prospect. The deal was to be a 5 year term, based on a 20 year amortization. The prospect had an offer in hand for a floating rate at 1 Month LIBOR + 2.50%. They told the bank that if they matched that rate, the deal was theirs. They thought that was way too cheap, so they countered with a 5 year fixed rate of 4.35%. With a cost of funds of around 0.30%, they felt that this rate got them a better spread, as they are fighting against margin compression.

Did they make the right decision? I plugged the loan into our Loan Builder calculator to find out.

The structure they proposed translated to a spread of 2.20% over LIBOR (the calculator used the swap market to translate a fixed rate loan to a floating rate loan). This is a VERY common mistake. We see banks loading up on 5 and 10 year fixed rate loans. They tell us that is "all the borrowers want." However, that is largely due to the fact that they are way over pricing shorter loans. They have "sticker shock" with the floating rate loans, and so are pushing borrowers to what is a much better deal out on the curve. This is all driven by the fact that a 3 handle (or even a 2 in this case) does not meet the hurdle of the "cost plus" pricing. (By the way, if this bank had wanted a 5 year structure, they could have made the floating rate loan at LIBOR + 250 and used an interest rate swap to make it a 5 year loan at 4.65%.)

2. A loan rate prices the deal for its prospective term - cost of funds is a historical number

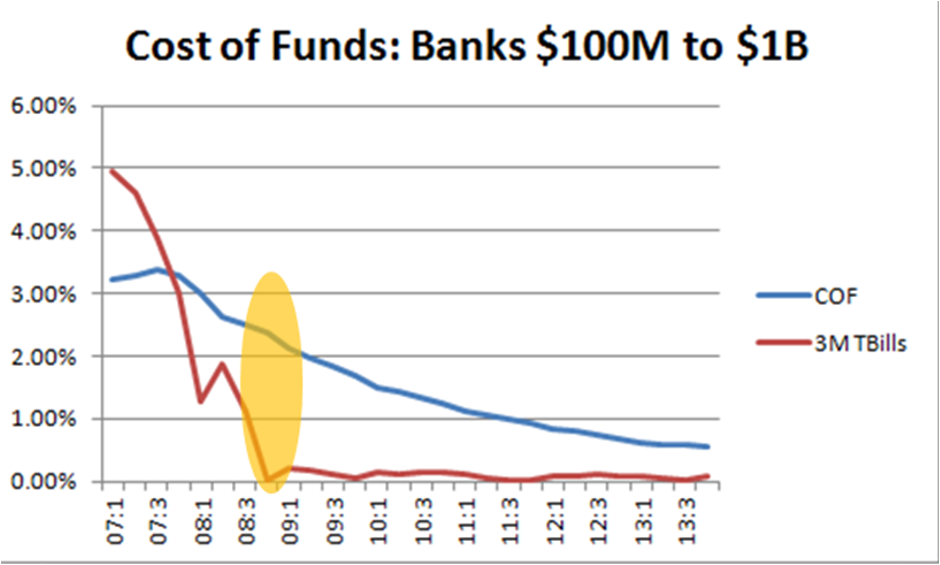

When we price a loan, we are setting the rate at which we will be compensated for all of those future cash flows. Cost of funds is a historical number. Even if you determine the current rate on all liabilities for cost of funds (as opposed to interest expense from accounting statements), that number was still built in the past as those liabilities were put on the books. This means that if rates rise, our cost of funds is built on lower rates, and we will be under-pricing our loans. Conversely, if rates fall, our cost is based on higher rates, and we will over-price our loans. A picture tells the story better than I can. This chart shows cost of funds for all banks between $100 million and $1 billion in assets (from FDIC call report data) compared to 3 month T-bill rates:

At inflection point sin the markets, these numbers can diverge quickly. The highlighted area shows how T-bills dropped quickly late in 2008 and early 2009 (as the financial world came unhinged and the stock market crashed). We entered a much lower rate environment, but our cost of funds had not yet caught up with the markets. If you continued to use "cost plus" you were likely way out of the market on most new deals. The loan market is simply too competitive now. Why would borrowers care if you have a high cost of funds? Do they want to pay more because of your funding structure? Do they care if you have high overhead that you need to cover? Conversely, should you charge much less than the market will bear for loans just because you have a funding advantage? Of course not - that advantage should show up as wider spreads and better earnings.

So, if using cost of funds is not right, how should we price loans? After all, we are not actually match funding every deal that comes through the door, are we? of course not. However, that does not mean we should ignore the yield curve.

This post is already long enough without jumping into a full blown methodology for pricing loans, so instead I will summarize. We need to price with the yield curve in context. If we can focus on what we call "Managed Spread" (that is, if we can consistently price on the right side of the curve at any given duration), then we can ensure that we have efficiently priced for interest rate risk. If we are taking more risk, we should be paid accordingly. If we are taking less risk, then we can and should expect a lower return. The yield curve tells us what the markets are expecting in terms of future rates, so using it to price is the best way for us to prepare our balance sheet for that future.

This has been an ongoing conversation for us with most of our clients, so there will be more posts to come on this topic. Stay tuned - a feel free to contact us if you want to discuss your specific situation.