What is an Interest Rate Swap?

by AMG

**note: this post is part of a series, "swaps basics." Click here for the complete list.

Learning about swaps and how they work in community financial institutions starts with a basic definition. An interest rate swap is defined as follows:

a popular and highly liquid financial derivative instrument whereby two parties agree to exchange interest rate cash flows based on a notional amount from a fixed rate to a floating rate (or vice versa) or from one floating rate to another.

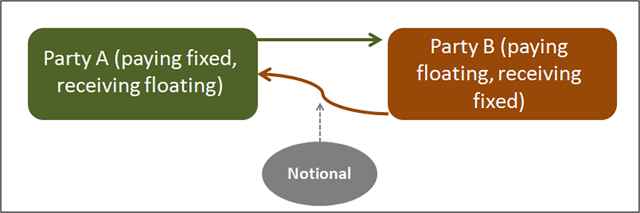

In pictures, a swap looks like this:

One of the main points of confusion as banks evaluate swaps is the understanding of how the notional amount of the swap works. If a bank enters into a $5 million swap, it is NOT on the hook for $5 million. The $5 million notional is only used as a way to calculate the amount of interest each side owes to the other. So, the bank is exposed by the interest rate * the notional, not the full notional amount.

The swaps market that community banks typically use is the US Dollar swaps market for LIBOR. Here is a screen shot of that swaps market from Bloomberg:

The rates listed for each term are the fixed rates that can be exchanged for LIBOR on a floating basis (in this case 3 month LIBOR). This is how swap rates are quoted - as an example, someone might say, "The 10 year swap rate is 3.09%." They are saying that in the current LIBOR swaps market, one side can pay 3.09% for 10 years, and in exchange they would receive 3 month LIBOR.

Swaps are settled on a net basis, meaning that at each settlement date, the accrued interest for the fixed rate and the accrued interest for the variable rate are both calculated. Whichever side owes then sends the funds. For example, in our 10 year swap, the fixed side dis 3.09%. The floating side is 3 month LIBOR, which is 0.26%. At settlement, the fixed payer would owe 3.09% - 0.26% = 2.83%. That 2.83% would be multiplied by the notional amount to determine the funds to be settled.

Here is the rest of this introductory series:

Introduction

Part 2: Counterparties

Part 3: Uses in Community Banks

Part 4: Risks and Benefits (coming soon!)

Part 5: Hedge Accounting (coming soon!)